Individual Bonds vs. Bond Funds

Bond funds and single bonds ultimately invest in the same thing but due to the nature of credit risks, maturities, and yields, the way investors own bonds can have different outcomes.

Buying bonds through an index, ETF, or mutual fund is the simplest way to gain broad fixed-income exposure. Investors will also get instant diversification by holding hundreds of bonds and bond types. The funds here come in different varieties where credit, duration, currency and country risks can be dialed up or down.

While investors in bond funds typically do not have to worry about liquidity, meaning they can sell shares of the fund whenever they want, there are indirect costs related to this. If other investors in the fund suddenly want their money, like in 2022, fund managers need to sell bonds to cover the liquidation. There are many cases where the manager would have to sell a bond at lower price than they would prefer. This tends to be the case when other investors cash out at the worst times. Depending how much needs to be sold, a manager might have to sell at a discount below market price.

But if the investor here owned single bonds, she would still have to sell at a steep discount if she wanted to sell her bonds. While it is an option to hold the bond until maturity and not take a loss, selling any bond prior to maturity be different than the face value. A single investor might not have liquidity issues that a fund manager experiences but selling single bonds can be daunting. While a bond market exists, it isn’t as active as the stock market. It isn’t uncommon for bond traders to call each other directly to execute a trade. Retail bond traders typically don’t have a direct line to a trade desk.

Both our fund investor and single bond investor would see paper gains and losses. We believe both types of investments have distinct advantages but will focus on how single bond portfolios can be managed with help. Consilio Wealth Advisors partners with a bond desk to execute trades and monitor credit ratings.

Why own bonds directly?

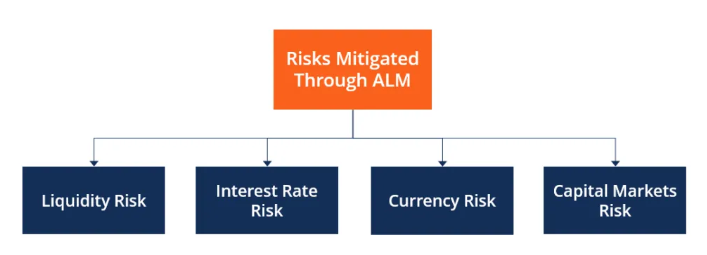

Endowments and pensions buy bonds and hold them to maturity, because they have very long time horizons. Price volatility can be ignored because these institutions employ an asset liability matching/management (ALM) strategy. Let’s say an endowment has a big payment due 10 years from now. They’ll calculate how much they need and will buy enough bonds that will mature in 10 years plus interest. Outside of default, an endowment can accurately predict how much they have at year 10. (I’m grossly simplifying things here. This strategy takes a lot of planning and work of a professional management team.)

This is accomplished through owning bonds directly. They know the face value, coupon, and maturity dates. With 10 years being such a long way out, a lot can happen where the risks below only apply if the bond needs to be sold prior to maturity. I get that most readers here aren’t endowments but there are some lessons to be taken from this strategy.

While holding the bonds, investors will see values fluctuate. Again, we aren’t selling anything so the fluctuations should not matter.

The biggest drawback of this strategy will be default risk. Although rare, a default can have an outsized downward impact on a direct bond portfolio. Where defaults in a fund are held to a minimum because there are hundreds of bonds to mitigate losses. Most defaults occurred in high yield bonds, or junk bonds, whose credit ratings already reflected high risk.

From the Corporate Finance Institute, “Historically, investment-grade bonds witness a low default rate compared to non-investment grade bonds. For example, S&P Global reported that the highest one-year default rate for AAA, AA, A, and BBB-rated bonds (investment-grade bonds) were 0%, 0.38%, 0.39%, and 1.02%, respectively.”

Investment grade bonds will experience a downgrade in credit rating before defaulting. Credit downgrades are risks but investors won’t lose all their investment here. Though not impossible, it is rare that an investment grade bond defaults before being downgraded.

Municipal bonds have an even better track record because their repayment ability is reliant on the tax base.

DISCLOSURES:

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

All investments include a risk of loss that clients should be prepared to bear. The principal risks of CWA strategies are disclosed in the publicly available Form ADV Part 2A.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.