Market Update: Waiting for the “All Clear”

October ended with a slew of pretty bad news:

Inflation is starting to creep into other parts of the economy like services.

There has been no indication of a slowdown in rate hikes.

There’s been more indications of a slowdown in the economy, meaning imminent recession.

China reaffirmed Xi’s power, which has been very unfriendly to business globally.

Earnings from the big tech bellwethers have been bad, save for Apple.

As expected, the market went up. Wait! The market went up??!!?

The obvious reason is there were more buyers than sellers throughout the month. What are buyers seeing?

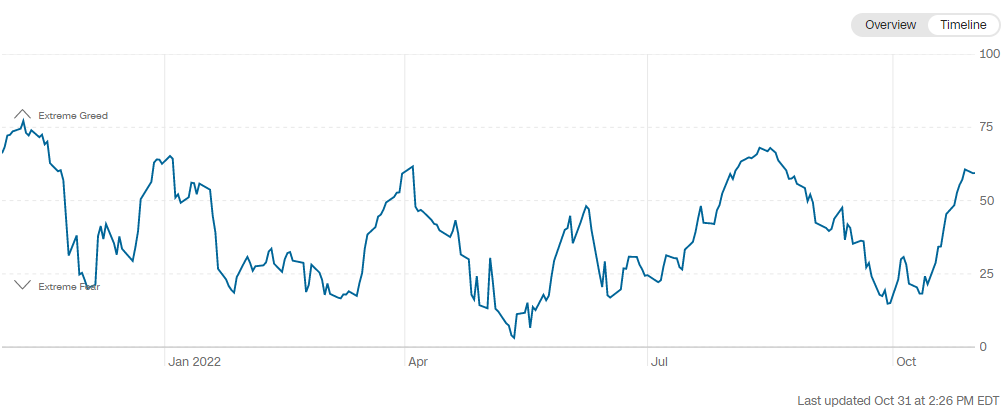

Up markets are good medicine for fear. The chart below is the fear/greed index. The lower the line, the more fear is baking into the markets. The higher the line, more greed is pricing in. Funny how up markets suddenly dissipate fear.

October has historically been known as the “bear market killer”, which means down markets have rebounded in October. The chart below shows that most bear markets have reached bottom during October, creating a new bull market.

There is also another technical tailwind that could propel markets in November. Mid term elections also have a consistent historical pattern of good market performance.

On average, the President’s party loses seats in both the House and Senate, creating a split government. While this may or may not be bad for the real world, the stock market loves this. When nothing gets done, a component of uncertainty is removed. No tax hikes or cuts, no new significant legislation that may help certain industries or harm others, typical government inaction. That’s what the stock market wants. Business as usual, which is predictable.

This polls suggest that the Republicans are favored to win the house and even odds to flip the senate.

This is the worst year to rely on historical patterns because 2022 has been the “historical pattern killer” and is carving its own history.

The biggest reason could be investors are anticipating a Fed pause in rate hikes. Other central banks around the world have been surprising with smaller hikes than anticipated. There have been very few clues about when the hiking may stop, but many believe that we are closer to the end.

Markets won’t wait for good news. Remember, once the news turns for the better (if it ever does), markets will be well off their bottom. Investors will see a shift in headlines and look back only to see, “I missed the bottom!”. Like October, this moment will come unexpectedly.

Buyers are seeing lower prices and are bargain hunting. They’re buying low.

DISCLOSURES:

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The information contained above is for illustrative purposes only.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

All investments include a risk of loss that clients should be prepared to bear. The principal risks of CWA strategies are disclosed in the publicly available Form ADV Part 2A.